Sipping a fruity drink while walking on the beach. Snuggling up with a good book in a quiet cabin in the woods. Filling your passport with stamps from exotic destinations. Finally learning how to play the guitar.

No matter how you envision your retirement, it’s a time when you can finally relax and enjoy the fruits of your labor. Retirement is a significant milestone and marks a major transition in life, and it is important that you plan ahead by laying a solid financial foundation so that you can truly make the most of it.

I recently spoke with Pattie Berkner, a Financial Advisor at Legacy Financial Partners, who says that not fully understanding what daily life will be like once your working years are over can be costly when it comes to achieving your retirement goals.

“Whether you are decades away from retirement or it’s right around the corner, it’s important to separate fact from fiction when it comes to planning for your post-work life,” Berkner explains.

A common belief about retirement is that that it will be significantly less expensive than your working years. For example, now that you’ve stopped working, expenses like commuting costs, work attire, lunches, and work-related social activities will decrease. And when you downsize or relocate to an area with a lower cost of living, your housing costs should be much lower. But the reality is more nuanced, and there are several factors to consider when evaluating the true cost of retirement.

Let’s take a look at some of the unexpected reasons your retirement expenses could be higher than you anticipated.

social security

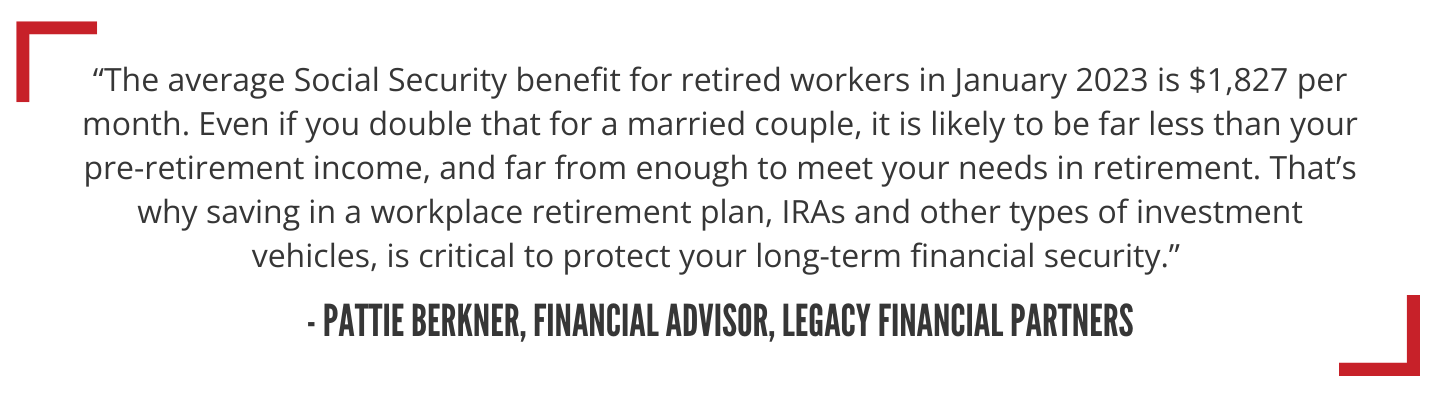

With advances in healthcare and better overall living conditions, people are living longer in retirement, and depending solely on Social Security might not be sufficient. Social Security benefits are designed to provide a safety net, but they're not intended to replace your full pre-retirement income.

.png?width=556&height=556&name=Pull%20Quote3%20(2000%20x%202000%20px).png)

On average, Social Security replaces about 40% of pre-retirement earnings for the average worker. This means you'll need additional sources of income to maintain your desired standard of living, especially if the number of years in retirement exceeds what you anticipated.

Healthcare

As individuals age, healthcare costs tend to rise. And while Medicare, the federal health insurance program for individuals aged 65 and older, is an essential component of retirement healthcare, it is not entirely free. Medicare Part A, which covers hospital stays, is usually premium-free for those who paid Medicare taxes while working. However, Part B (covering outpatient care) and Part D (prescription drug coverage) come with monthly premiums, deductibles, and copayments. High-income retirees may face higher premiums for Medicare Part B and Part D, known as Income-Related Monthly Adjustment Amounts (IRMAA). These additional costs can be significant for wealthier retirees.

“Medicare is a critical benefit for retirees, but it wasn’t designed to cover everything,” Berkner explains.

As such, many retirees opt for supplemental insurance plans like Medigap or Medicare Advantage to cover expenses not paid for by original Medicare. These plans come with additional premiums and potentially out-of-pocket costs, depending on the plan and coverage. Traditional Medicare does not cover most long-term care services, such as nursing home care or assisted living. Retirees who require these services may need to purchase separate long-term care insurance or explore Medicaid options.

In addition, those retiring before their 65th birthday may face the challenge of securing affordable health insurance until they qualify for Medicare. COBRA coverage, private insurance, or coverage through a spouse's plan may be necessary.

Long-Term Care and Assisted Living

The need for long-term care or assisted living facilities is a significant expense that often arises in retirement. These costs can be substantial and are not typically covered by standard health insurance.

Inflation and Cost of Living

Over time, the cost of goods and services tends to increase due to inflation. This means that retirees may face higher prices for everyday expenses. And while Social Security's cost-of-living adjustments (COLAs) are meant to help benefits keep pace with inflation, these adjustments may not always fully account for rising costs in specific areas, like healthcare and housing.

Government Policy Changes

Social Security benefits are subject to potential changes in government policies, and factors like inflation, economic conditions, and policy decisions can impact benefit amounts. Relying solely on these benefits without a backup plan could leave you vulnerable to unexpected reductions.

Travel and Leisure Activities

Retirement often frees up more time to pursue other interests which can bring joy and fulfillment, but they can also come with associated expenses. Costs for meals out at restaurants, hobbies, cruises, or extended trips abroad can add up quickly.

Home Maintenance and Renovations

As homes age, they often require maintenance and repairs. Additionally, retirees may choose to renovate or make modifications to their homes to accommodate changing needs.

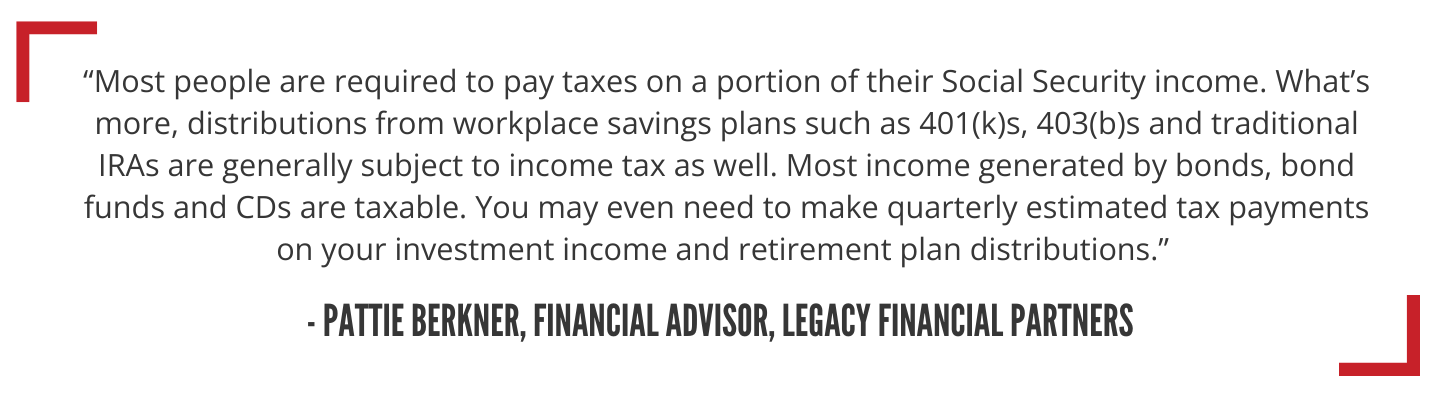

Taxes

While you may save on property taxes and utilities when you downsize or relocate, new costs may arise such as homeowner association and facility fees. Also, depending on the sources of your retirement income, you may still be subject to federal and state taxes. It's crucial to understand the tax implications of various income streams in retirement.

THE bottom line

When planning for your retirement, you should do a thorough assessment of all your potential costs, and then create a financial strategy that addresses them. Understanding that retirement life may not be inherently less expensive, you can enter this well-deserved phase of life with realistic expectations and financial preparedness.

Note: This article is not intended to replace a conversation with your financial planner who knows your unique situation. If you are looking for a financial planner, feel free to contact Pattie Berkner. If you are a K&J driver we also have additional financial planning resources that we can give you!